- Capital Call by OneFund

- Posts

- Capital Call 2023 Finale: Middle Market PE Update

Capital Call 2023 Finale: Middle Market PE Update

A bi-weekly newsletter from LPs for LPs, covering the latest and greatest from across the private markets

John Bailey

December 28, 2023

It’s been a great first year of Capital Call! Thank you all for reading and engaging with us.

The mission of Capital Call is to deliver concise, top-notch insights and updates from the private markets tailored to what matters for LPs.

This week we will be looking at:

Updates on the Q3 PE Middle Market

Fundraising updates and VC/PE reports

GP Perspectives from Sheldon Stone, Henry McVey, and Michael Annunziata

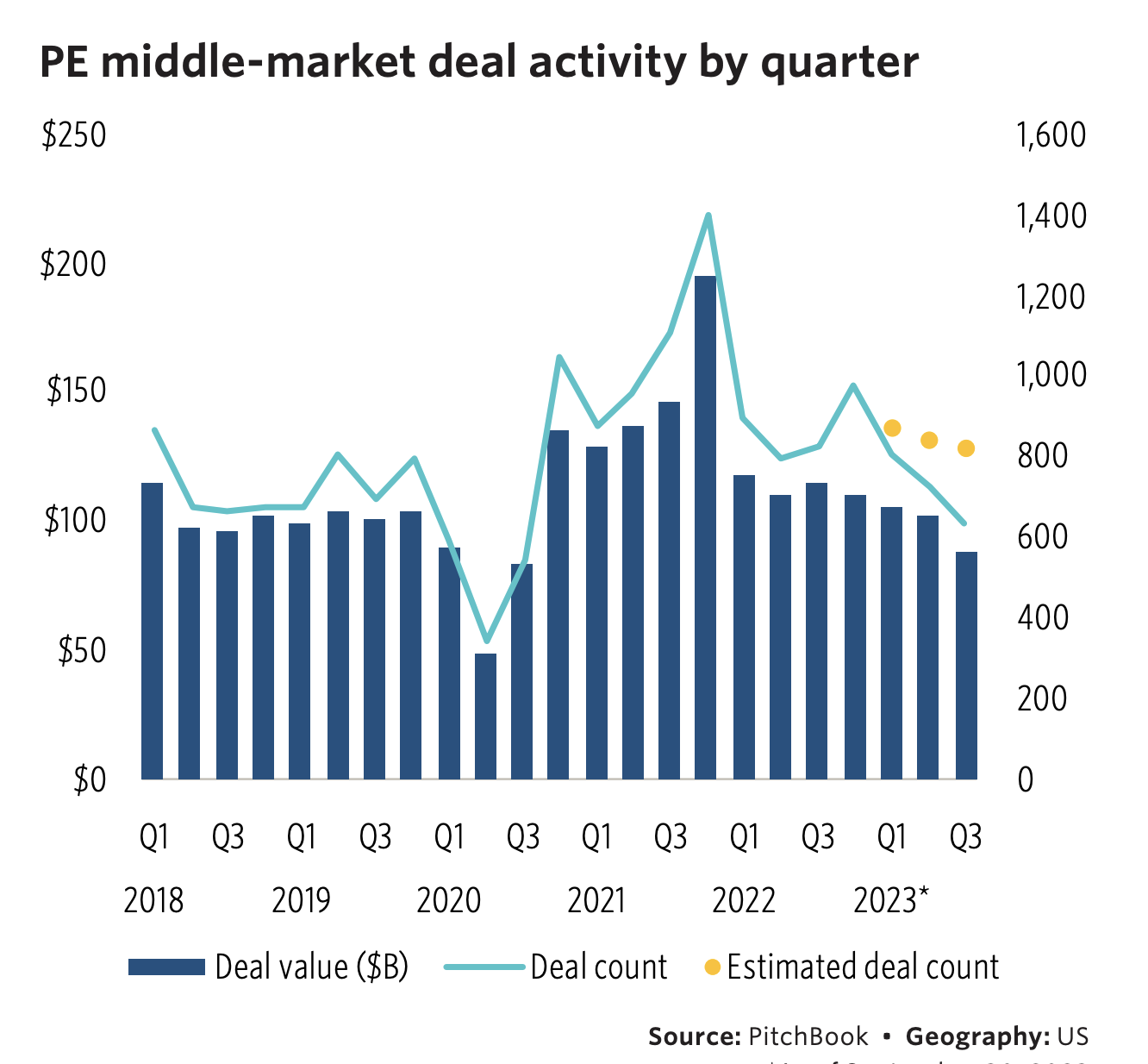

Q3 Middle Market PE Update

Last week, Pitchbook released its Q3 middle market private equity report, finding that the slowdown in PE megadeals is finally trickling down to the middle market. Last quarter, mid-market PE witnessed a three-year quarterly low in deal volume and a 26% quarter-over-quarter decline in exit value.

Though these results are disappointing to investors, this is contrasted by the sector’s continued strength in performance and fundraising. This leads Pitchbook to retain their prediction of a sustained recovery in middle-market PE deal activity, concluding Q3 as a setback that will delay the rebound by another quarter rather than the start of a longer-term slump.

In today’s newsletter, I’ll cover the causes of Q3’s slowdown and dive into the future of middle market PE, highlighting the insights and predictions that matter most to LPs.

Debt Accessible, but Deal Market Stalls

The slowdown of megadeal activity is primarily driven by significantly reduced access to debt, where 2023 observed a glass ceiling of around $2 billion for large leveraged buyouts (LBOs). Since the middle market operates well below the $2 billion limit, there were fewer issues using debt to drive deals.

The sector is actively serviced by the various and growing number of private lenders and credit funds, whether they are private debt funds backed by institutions, listed business-development companies (BDCs), or the newer types of entities backed by retail investors. These 1,300 institutions collectively represent ~$1 trillion in the US alone, and almost all have expressed support for lending to the mid-market.

So what caused the minor setback in Q3 then for MM deals? Primarily, the supply of willing buyers and sellers shrank during Q3. The interest-rate shock in Q3 resulted in the 10-year treasury yield rising a full 1% to a near 15-year high. This caused deal economics to falter and negotiations to stall during the quarter, putting many deals on hold. This could change meaningfully in 2024 however as the fed expects to be cutting rates.

Because of this, GPs and LPs alike should note the keyword is “on hold” as most of these paused deals are expected to resume following rate cuts. The current climate appears promising, with the Fed deciding to hold rates constant at 5.25-5.50% during their December 13th meeting and many analysts predicting 100 basis points of rate cuts spread across 2024.

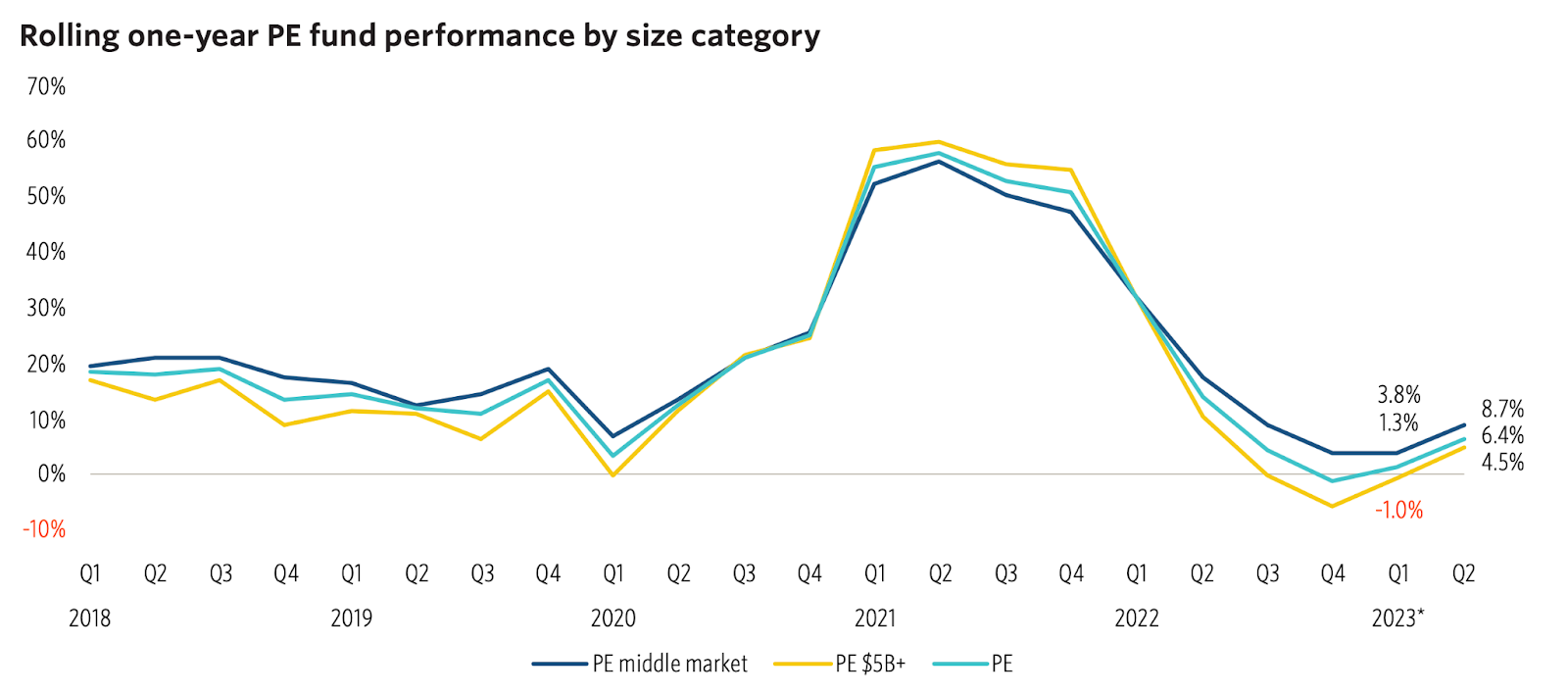

Fundraising & Performance Prove Resilient

The latest performance data shows middle-market buyout PE outperforming megafunds for over four consecutive quarters. As seen in the chart, middle-market PE achieved 8.7% IRR vs. megafunds’ 6.4% IRR over a one-year horizon. It will be interesting to see how this persists though as the economy improves. My hunch is that it will reverse.

Returns of the two market segments are converging as the benefit of public market rallies and scale are trickling to larger funds. This typically aids larger exits either through IPOs or justifying enhanced exit multiples, which are usually discounted in the mid-market.

As a result of strong performance, middle-market dry powder reached a record $475 billion due to successive rounds of strong fundraising. Analysts notice that new managers are being given more opportunities than last time the PE market was under stress, as long as they can raise over $100 million and demonstrate a differentiated strategy and higher alpha than other buyout offerings.

How Should LPs Think Through This?

Q3 middle-market PE market data may appear conflicting, with declines in deal activity and exit value happening at the same time as strong fundraising and relative outperformance. This can reiterate the historical trend of strong fund vintages coming after difficult economic conditions.

For example, fund vintages in 2009/10 have far outperformed their peers, which may also be the case for 2023/24 vintages. A flood of deal activity will occur once macro conditions normalize, but LPs should still prioritize outperformance through differentiation and secular tailwinds rather than merely ride the rebound. As always, diversifying by when you invest in PE is similarly important to diversifying where you invest.

Updates from Across the Ecosystem

Fundraising

Reports

GP perspectives:

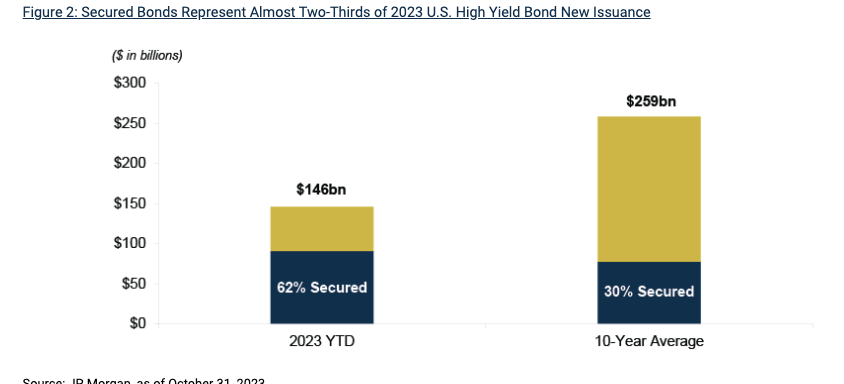

Sheldon Stone (Portfolio Manager, Oaktree)

In Oaktree’s latest analysis on credit markets, portfolio manager Sheldon Stone notices a significant rise in the percentage of secured bonds. Secured bonds, which provide more downside protection in the event of a restructuring compared to unsecured notes, now comprise 62% of the market compared to their 10-year average of 30%.

What this means for LPs is that credit market fundamentals are healthy and are geared towards downside protection. This corresponds with lower Debt / EBITDA of 4.0x, meaning companies are taking less leverage than before. Due to this credit market health, defaults are unlikely to start a chain of recessionary reactions as seen in past crises.

Henry McVey (Partner, KKR)

In his latest memo, aptly named “Glass Half Full”, Henry McVey believes that general investors are “locked into the paradigm that the S&P 500 is trading at lofty headline valuations and the U.S. economy is topping out and headed for a hard landing.” As a result, he believes they are “sitting idle, as they feel there is little to no value in the market beyond cash.”

He believes this couldn’t be further from the truth, as many sectors need capital to grow or reposition their businesses alongside enormous opportunities in public-to-private and carve-out transactions.

These trends, along with the opportunity set to invest behind some of the biggest mega-themes such as decarbonization, digitalization, and deglobalization keep the “glass half full” for global allocators like KKR.

Michael Annunziata (Founder, Also Capital)

Annunziata supports the investment trend of exceptional fund vintages coming out of difficult times. He brings up the important point that alpha generation should be through conviction on strategy and team operators rather than momentum alone.

It’s often worth paying a premium to secure quality for the long term as compounding returns will far negate higher upfront costs.

About OneFund

OneFund is democratizing access to Private Equity and Venture Capital for everyday investors. We partner with the world's top PE & VC funds to offer investment options without the million-dollar minimums.

If you would like to follow what we are doing, get more regular updates directly from the team, or become a member, schedule a call!

Reply