- Capital Call by OneFund

- Posts

- Finding M&A Success in a Down-Market

Finding M&A Success in a Down-Market

A bi-weekly newsletter from LPs for LPs, covering the latest and greatest from across the private markets

John Bailey

February 23, 2024

Calling all LPs! Thanks for joining me (John Bailey, Co-Founder at OneFund) for another edition of Capital Call.

The mission of Capital Call, our bi-weekly private equity newsletter from LPs for LPs, is to deliver concise, top-notch insights and updates from the private markets tailored to what matters for LPs.

This week we will be looking at:

Navigating M&A Opportunities in a Down-Market

Fundraising updates and PE / Supply Chain reports

GP Perspectives from Jon Gray, Hussein Adatia, and Kate Gribbon

Private Market Movements

Finding M&A Success in a Down-Market

Last year’s M&A market faced challenges due to a significant valuation gap between buyers and sellers, along with other obstacles such as high-interest rates, macroeconomic uncertainty, and regulatory risk.

Most market participants expect a widespread recovery in 2024, beginning with rate cuts in the next few months, but investors may have to continue operating in a down-market for the first half of the year.

This raises the question, how can investors find M&A success in a down-market? According to Bain’s latest report, the most successful acquisitions in 2023 involved strategic deals in sectors like healthcare, life sciences, and energy. The Americas market also remained exceptionally steady compared to Europe and Asia, providing a stable backdrop for acquisitions.

In this week’s newsletter, I’ll unpack Bain’s analysis of how to succeed in a down-market and where to look for deals, diving into the insights that matter most to LPs.

Tech on Pause while Vertical Healthcare, Life Sciences, and Energy Deals Prosper

Starting with sector focus, a primary driver of an investor's M&A opportunities, acquirers in energy, healthcare, life sciences, media, and retail saw significant deal flow in strategic M&A whereas tech was responsible for most of 2023’s decline.

The common theme that emerged was vertical acquisitions, where companies turned to M&A to reshape their future strategic goals. This was seen with automakers securing supplies for electric vehicles, insurers expanding into risk prevention, healthcare pursuing increased scope of offerings, and media companies merging content and distribution.

Cross-border activity is another area of growth, with 34% higher deal value in 2023 compared to the prior year. US buyers are increasingly pursuing international acquisitions in favorable, complementary markets.

However, despite the increased opportunities in these areas, it was not enough to offset the tech sector’s M&A pause. Tech deal value collapsed to roughly 45% as valuations tumbled to roughly half of 2021’s highs.

There is undoubtedly ongoing demand for high-quality, profitable tech assets, but the higher-for-longer interest rate environment changes the deal calculus for many tech deals. Many tech firms were built on growth over profitability in the COVID years, but the current macro environment values the opposite.

GPs and LPs involved in tech private equity should emphasize profitability-enhancing initiatives rather than lofty growth goals over the near term to ensure favorable exit values are realized.

Tech is still experiencing double-digit revenue growth in many verticals due to unprecedented digital tailwinds, and investors can still pursue attractive M&A in the down-market as long as they understand the market shift towards profitability.

Frequent Acquirers Win in the Long-Term

Seeing an M&A down-market may convince GPs and LPs alike to sit on the sidelines until conditions improve, but Bain’s research finds that firms who can pursue M&A throughout all market cycles create outperformance.

As seen above, most frequent acquirers were able to complete an acquisition both during COVID-19 and through the current period of higher rates. Frequent acquirers that stayed active are pulling far ahead of less acquisitive or inactive companies in terms of long-term total shareholder returns.

Bain’s research shows that the benefits of frequency are only increasing over time, signaling a longer-term fundamental shift. GPs that invest across cycles can deploy tested and tailored toolkits to transform their businesses and learn how to keep portfolio companies dynamic across environments, ultimately emerging as winners.

LPs looking to commit to long-term relationships with GPs should ensure they are actively investing and learning throughout the current down-cycle, and not merely sitting on the sidelines until rates decline.

Updates from Across the Ecosystem

Fundraising

Reports

GP perspectives:

Kate Gribbon (Head of Financial Sponsors, Investec)

Kate Gribbon, Head of Financial Sponsors at Investec, notes that PE valuations decreased in her latest market analysis. Below, I’ve summarized her insights and highlighted the most relevant points for LPs to consider.

Expectations for deals were set too high

This led to unrealistic bid/ask spreads and a decline in deal activity as valuations adjusted to a new normal.

Sellers are impacted by macroeconomic uncertainties

As we’ve discussed, high inflation and interest rates resulted in pressure on profitability.

Higher borrowing costs

Higher interest rates are obvious, but tighter lending terms are also impacting deal valuations.

GPs face liquidity pressures

Many GPs accepted lower valuations to generate liquidity for LPs, although this doesn't necessarily result in losses.

Longer fundraising timelines

Slower fundraising and deal completions are observed, affecting distributions back to limited partners who prioritize liquidity over returns.

These factors were major hurdles to PE investors in 2023, but they are not expected to be as significant in 2024. Looking ahead, as deal volumes increase due to rate cuts, valuations are expected to rise gradually and businesses will be willing to engage in transactions as they adjust to the new market conditions.

As always, opportunities remain in the market despite the current obstacles, and now may be the best time to invest. GPs that show the resilience and adaptability to follow through with their M&A goals will be well-positioned to benefit from the coming market recovery.

Jon Gray (President, Blackstone)

Jon Gray, President of Blackstone, believes now is the best time for GPs to pursue acquisitions. He states, “You can see the light at the end of the tunnel, but it’s not yet priced into the market.”

Gray is referring to inflation coming down sharply, incoming Fed rate cuts, and resilient organic growth of portfolio companies. His investing focus area for this year will involve private credit, alternative capital solutions, and private equity investing in sectors with long-term tailwinds such as energy transition, digitization, healthcare, and travel & leisure.

To gain deeper insights, I recommend you watch his full market analysis here.

Hussein Adatia (Portfolio Manager, Westwood)

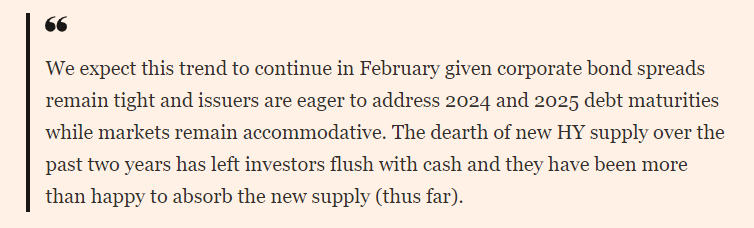

In a recent article, Hussein Adatia comments on the low spreads on high-yield bonds:

High-yield bonds are typically used by PE investors to finance LBOs. The spreads refer to the difference between the rate of the high-yield bond compared to the treasury rate. For example, the current 7% rate on high-yield bonds compared to the 3.5% yield of a long-term treasury represents the current spread of 350 basis points.

This is abnormally low compared to the 800 basis point spread expected during times of recession risk, and Adatia believes this trend will continue as strong GDP growth, falling cyclical risk, and expected rate cuts fuel credit investor demand for high-yield bonds.

This is good news for private equity investors as they aren’t expected to be further impacted by rising costs of debt, allowing deal activity to recover. GPs and LPs alike can expect stabilized cost of debt rates for the first half of the year, followed by declining rates as Fed cuts are implemented.

About OneFund

OneFund is democratizing access to Private Equity and Venture Capital for everyday investors. We partner with the world's top PE & VC funds to offer investment options without the million-dollar minimums.

If you would like to follow what we are doing, get more regular updates directly from the team, or become a member, schedule a call!

Reply