- Capital Call by OneFund

- Posts

- Global M&A Recovery Predictions

Global M&A Recovery Predictions

A bi-weekly newsletter from LPs for LPs, covering the latest and greatest from across the private markets

John Bailey

February 09, 2024

Calling all LPs! Thanks for joining me (John Bailey, Co-Founder at OneFund) for another edition of Capital Call.

The mission of Capital Call, our bi-weekly private equity newsletter from LPs for LPs, is to deliver concise, top-notch insights and updates from the private markets tailored to what matters for LPs.

This week we will be looking at:

Some Global M&A Recovery Predictions

Fundraising updates and Macro/PE reports

GP Perspectives from Eyal Malinger, Rowan Bamford, and Verdun Perry

Private Market Movements

2024 Fed Easing Cycle Projected to Fuel Global M&A Recovery

In 2023, the global M&A market experienced its second weakest year in a decade, with $3 trillion worth of deals marking a 15.8% decrease from 2022, according to Pitchbook.

Despite this decline, most analysts believe the market turbulence is behind us, and that the most recent quarter showed significantly improved volumes. Additionally, a potential nearing Fed easing cycle is expected to further drive a recovery in activity.

Looking forward into 2024, the market consensus remains bullish regarding M&A activity and most analysts retain the view that a market recovery this year is imminent. In this week’s newsletter, I’ll dive into Pitchbook’s most recent M&A data and unpack M&A recovery predictions and the insights that matter most to LPs.

Strong Q4 and Middle-Market Despite Broader M&A Underperformance

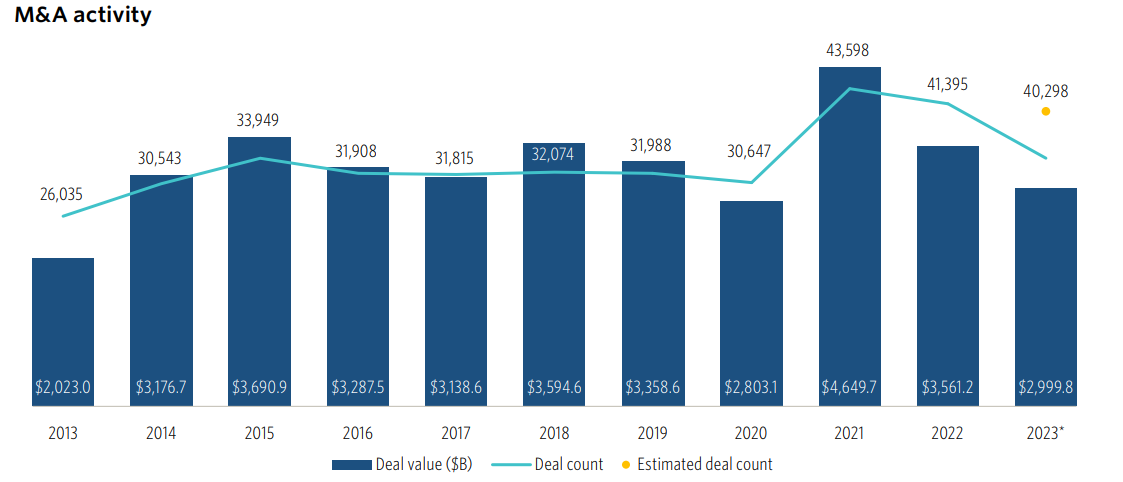

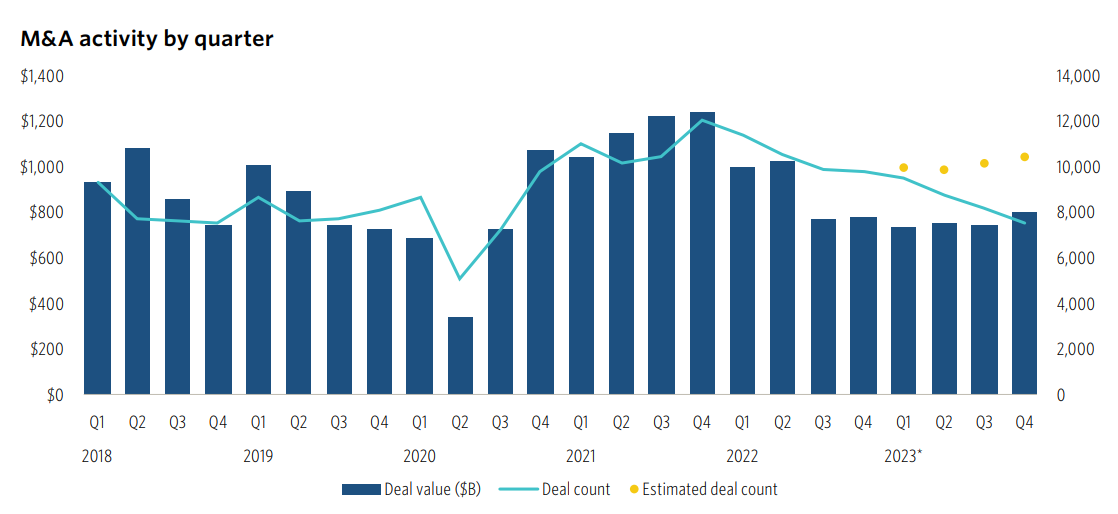

First, it’s important to note that while 2023 was a weak year in terms of M&A deal value, it was an exceptionally good year in terms of deal count. Looking at the chart above, the 40,000+ M&A deals in 2023 ranked as the third highest on record, only surpassed by the deal frenzy years of 2021 and 2022.

This is because most deals are being executed in the middle market, where lower leverage is more common and high debt costs are not as much of a hindrance. Middle market M&A is healthy and performing strong, while large and mega-size deals likely won’t fully recover until debt costs ease.

But even with record-high interest rates, the M&A market is already showing signs of recovery. As seen in the chart above, Q4 M&A data far exceeded expectations with a deal value increase of 17.8% year-over-year and an even greater 35.9% quarter-over-quarter.

This indicates that acquirers are finding the organic value drivers and operational improvement opportunities to justify larger acquisitions, counterbalancing the drag on returns brought by higher cost of debt.

A recovery may already be underway based on Q4’s strong data, and rate easing in 2024 will only bring further optimism for deal activity over the coming quarters.

Fed Easing Cyle Projected to Commence Early 2024

Analysts predict that the two-year anniversary of the Fed’s historic rate hike cycle will mark a significant milestone that signifies the end of rate hikes. If predictions hold, March 2024 will be the start of a new cycle of Fed easing.

This would provide relief to GPs strained by 12% or higher borrowing costs and help the $1.6 trillion in PE dry powder get back into motion, spurring a significant wave of deal activity.

2024’s outlook for deal activity appears promising, but investors should still be aware that the global economy could land hard and not soft like the US has.

Overall, LPs can expect stronger deal flow in 2024 with GPs deploying more dry powder, but this doesn’t mean GPs should be waiting until conditions improve to pursue opportunities. GPs who can execute successfully in this environment are able to drive strong operational transformation, and rate easing will only add to their performance.

Even with rate easing, relying on financial engineering to drive returns will not return and LPs should continue to build relationships with GPs who are strong operators to achieve outsized returns.

Updates from Across the Ecosystem

Fundraising

Reports

GP perspectives:

Eyal Malinger (Partner, Resurge Growth Partners)

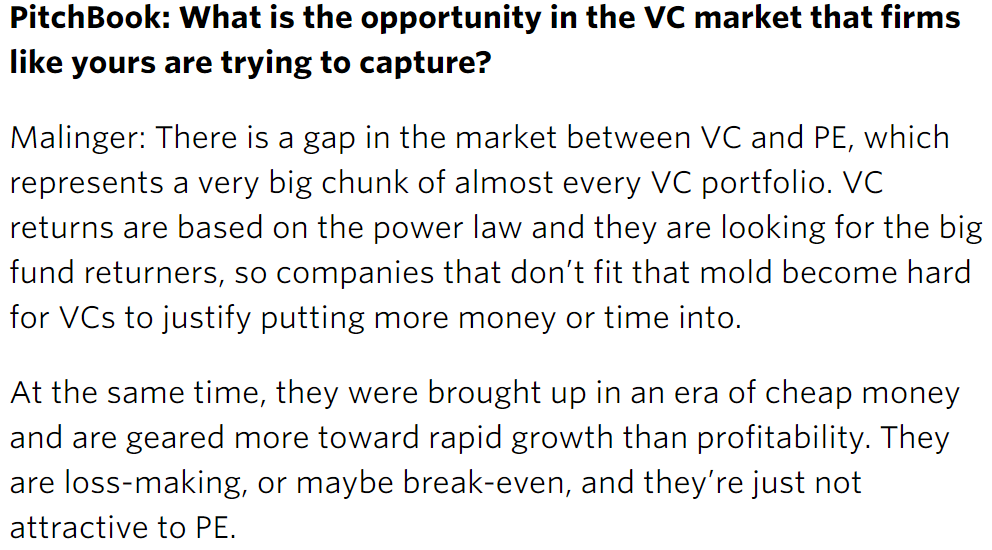

Eyal Malinger, Partner at Resurge Growth Partners, points out a market gap in the VC and PE industry in a recent interview.

Many companies are stuck in a limbo between VC and PE since they aren’t growing fast enough to achieve the 10x or higher returns VCs pursue but are also not profitable enough to attract PE money.

This provides opportunities for GPs to acquire controlling stakes in these companies and help them transition from a path of hypergrowth to a more sustainable profitability model that can attract PE exits. Successful execution will require VC skills, such as understanding how cap tables and VC boards work, as well as PE operating experience to achieve improved profitability.

GPs and LPs involved are theoretically then rewarded with attractive risk-adjusted returns, balancing profitability and growth, and the ability to gain investment exposure to VC-like companies in the currently frozen VC deal market. I recommend reading Eyal’s full interview here for a full analysis of the strategy.

Rowan Bamford (President, Liberty GTS)

Rowan Bamford, President at Liberty GTS, predicts that a 1.5-2% reduction in rates will be needed for a full M&A recovery in a recent analysis. Rowan believes the current difficult market conditions will persist for the first half of 2024, and then rate easing will drive a recovery thereafter. While this may hold true for M&A markets, considering the strong US job market, the fed may decide this is not needed.

Due to this, acquisition teams will need to be smart and resourceful in underwriting for the next quarter or two and cannot merely rely on easing rates.

Rowan also believes 2024 acquisitions will still see lower multiples than the staggering 2022 valuations. Acquirers will consider pricing dynamics heavily in M&A, and scrutinize more subjective areas such as intangible assets.

As a result, LPs should ensure GPs are applying appropriate acquisition multiples this year, rather than take more risks due to optimistic macro outlooks.

Verdun Perry (Global Head of Strategic Partners, Blackstone)

Blackstone’s Verdun Perry is very bullish on deal activity in 2024, especially in the secondaries space. In 2000, the secondaries market was merely $1.3b in deal volume, but Blackstone estimates the market to exceed $130 billion this year.

This is mostly due to LP’s increased awareness of the market, where 80% of LPs are familiar with secondaries today compared to near-zero not too long ago. Blackstone estimates the secondaries portion of all PE deal value to increase as LPs continue to familiarize themselves with structuring secondaries deals.

If you are not familiar with secondaries, or would like to hear a more in-depth analysis of the market, I recommend taking thirty minutes to listen to Perry’s podcast.

About OneFund

OneFund is democratizing access to Private Equity and Venture Capital for everyday investors. We partner with the world's top PE & VC funds to offer investment options without the million-dollar minimums.

If you would like to follow what we are doing, get more regular updates directly from the team, or become a member, schedule a call!

Reply