- Capital Call by OneFund

- Posts

- Middle Market Deal Making Continues Momentum

Middle Market Deal Making Continues Momentum

A bi-weekly newsletter from LPs for LPs, covering the latest and greatest from across the private markets

John Bailey

March 22, 2024

Calling all LPs! Thanks for joining me (John Bailey, Co-Founder at OneFund) for another edition of Capital Call.

The mission of Capital Call, our bi-weekly private equity newsletter from LPs for LPs, is to deliver concise, top-notch insights and updates from the private markets tailored to what matters for LPs.

This week we will be looking at:

Middle Market Momentum

Fundraising updates and Macro / Market reports

GP Perspectives from Jeff Hammer, Robert Horn

Private Market Movements

Middle Market Deal-Making Continues Momentum

In the latest quarter, US middle-market PE dealmaking saw growing momentum, with both buy-side and sell-side activity increasing in deal value and count according to Pitchbook’s most recent middle-market PE report.

This was driven by continued positive drivers for the middle market including strong fundraising, returns outperformance, and efficiency in distributing capital to investors. In addition, some of this growth came from rescue capital, restructurings, and other distressed asset transactions.

In today’s newsletter, I’ll dive into Pitchbook’s middle market report and uncover the insights and trends that matter most to LPs.

Deal Activity, Fundraising, and Distributions Accelerate

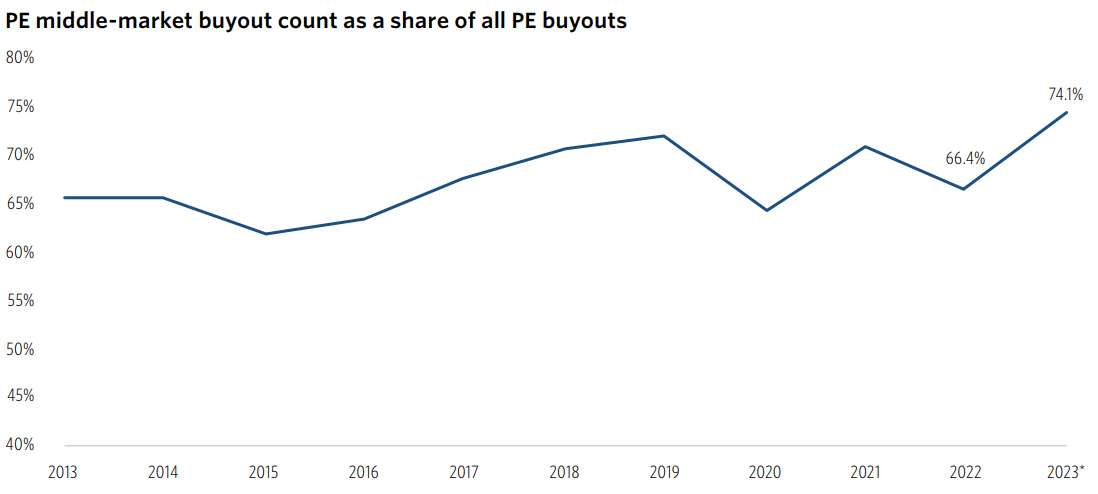

Currently, the middle market accounts for 74.1% of all deal count surpassing the 66.4% figure of 2022 as deal count rose 4% from 3,549 in 2022 to 3,689 in 2023.

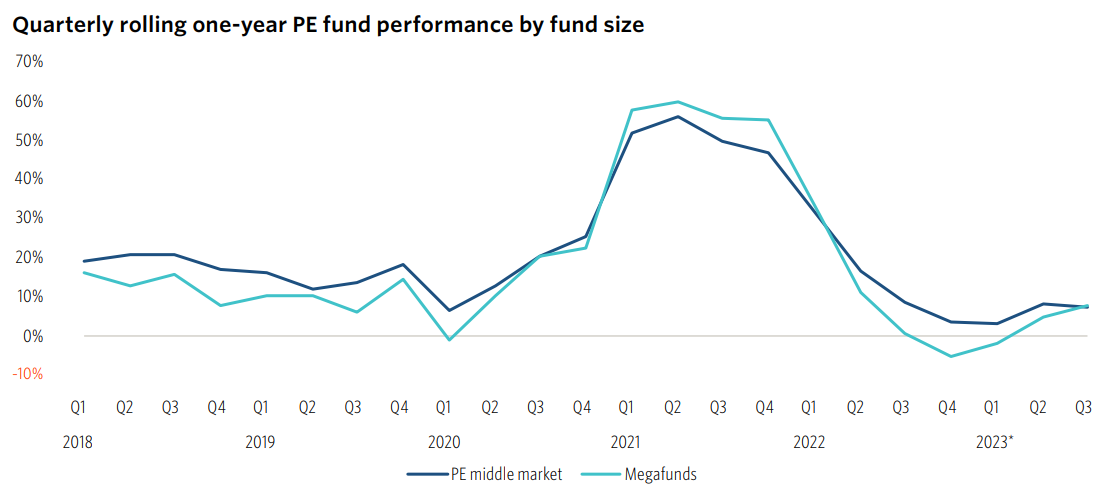

These statistics are largely due to the recent, relative outperformance of the middle market compared to megafunds, as smaller transactions are more feasible to structure in times of high rates. Despite this, buyout value still declined by 18.9% in 2023, though not as severe as the broader PE market's decline of 32.7%.

Though the market is performing well in this difficult environment, a full recovery has not materialized yet and investors will likely need to wait until macro conditions further normalize. LPs can continue to expect stable, moderate returns with opportunities for outsized performance in the coming years.

Middle market PE has outperformed megafunds for most of 2022 and 2023, but returns are now equalizing as the public market rally benefits large investors more. Middle-market funds have also benefited from the rally as valuation growth extended to small and mid-cap companies.

Where middle market managers really shone last year was on the distribution front. 2023 data shows mid-market managers received $66.3 billion in contributions and distributed $88.7 billion, resulting in a positive inflow of $22.4 billion to investors.

In contrast, megafunds experienced contributions nearly doubling their distributions, leading to a net outflow of -$30.0 billion. While this isn’t necessarily indicative of performance, it does highlight the comparative ease mid-market managers have had in exiting portfolio companies compared to larger funds in the last year.

For LPs, greater distributions increase DPI (Distributions to Paid-in-Capital), even if IRR appears the same. LPs should consider both IRR and DPI when evaluating investments, as DPI is a more realistic representation of cash returns. However, IRR is also necessary as it captures the time component of returns as well as unrealized returns.

Opportunities for Rescue Capital and Distressed Transactions

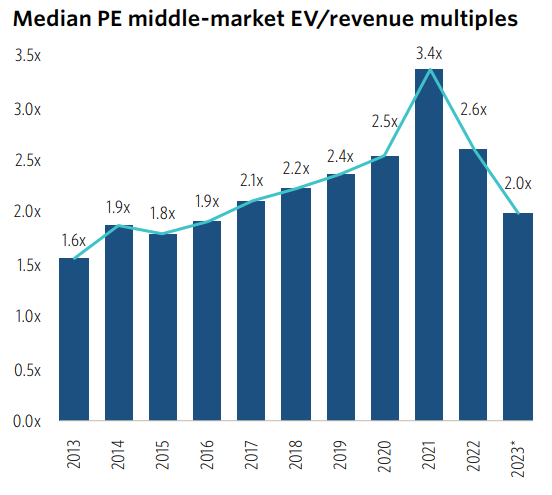

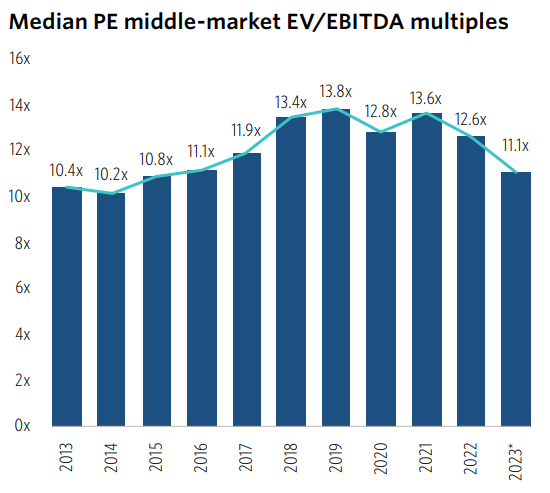

The majority of growth seen last quarter in mid-market PE was driven by positive trends, but some of it was also due to growth in rescue capital and distressed transactions. As seen above, valuations are down both in terms of EV/EBITDA and EV/revenue, providing opportunities for PEs to acquire at discount prices.

This was reflected in numerous restructurings in the recent quarter, where poor-performing or near-bankrupt companies were acquired with a turnaround plan. Though this activity will dissipate as economic conditions recover, it keeps valuations from falling further and provides opportunities for LPs and GPs.

Looking forward, the overall industry's participation in a total recovery depends on an increase in exit activity, which continues to remain low due to market challenges. Investors anticipate this will be addressed by the forecasted rate cuts and strengthening of the public market, although uncertainties will persist in the near term. LPs and GPs alike who are confident in the expected market recovery can take advantage of lower valuations today, including distressed opportunities, to drive greater returns.

Updates from Across the Ecosystem

Fundraising

Reports

GP perspectives:

Jeff Hammer (Global Co-Head of Secondaries, Manulife Investment Management)

With the secondaries market heating up, Jeff Hammer provides useful insights on how GPs diligence secondaries transactions in a recent Q&A. Usually, the original GP will still have a major stake in a continuation vehicle, so it is important to diligence the sponsor and their asset management framework.

It’s also crucial to determine whether the original GP is simply looking to cash out, or if they are truly looking to extend the holding of that asset. The latter is beneficial as they are typically more reliable as a steward of the asset.

Finally, asset-level diligence is conducted similarly to a typical buy-out transaction. I recommend reading Hammer’s full analysis to gain a more comprehensive view.

Robert Horn (Global head of Sustainable Resources, Blackstone)

Robert Horn provides an example of a simple, effective private equity investment framework in a recent Blackstone report. Here, they identified a megatrend, decarbonization in this case, and provided the portfolio company with everything they required for growth.

This includes providing capital, assisting with debt financing, facilitating customer interactions, and offering industry expertise. The integrated approach allowed the company to grow its asset base by 6x and create enormous value for Blackstone.

Overall, Horn highlights the growing necessity of value creation in PE and how it can be achieved using connections, operations, industry experience, and other levers. GPs will need to take integrated approaches, creating value in multiple workstreams, if they want to succeed in today’s landscape rather than merely buy and hold assets.

About OneFund

OneFund is democratizing access to Private Equity and Venture Capital for everyday investors. We partner with the world's top PE & VC funds to offer investment options without the million-dollar minimums.

If you would like to follow what we are doing, get more regular updates directly from the team, or become a member, schedule a call!

Reply