- Capital Call by OneFund

- Posts

- Private Market Expected Return Themes

Private Market Expected Return Themes

A bi-weekly newsletter from LPs for LPs, covering the latest and greatest from across the private markets

John Bailey

January 24, 2024

Calling all LPs! Thanks for joining me (John Bailey, Co-Founder at OneFund) for another edition of Capital Call.

The mission of Capital Call, our bi-weekly private equity newsletter from LPs for LPs, is to deliver concise, top-notch insights and updates from the private markets tailored to what matters for LPs.

This week we will be looking at:

Private Market Expected Return Themes Over the Next 5 Years

Fundraising updates and Macro/PE reports

GP Perspectives from Howard Marks, Matt Nord, Andrew Schwedel, and James Root

Private Market Movements

Private Market Expected Return Themes

As analysts and researchers forecast their outlooks for 2024, a common theme emerging is that this will be a transition year with major regime changes in private markets. Key themes such as fiscal impulse, labor costs, energy transition, and global supply chain restructuring will continue to drive asset allocation strategies.

In today’s newsletter, I’ll discuss a bit about how expected returns in private markets are evolving, diving into market analysis by KKR to uncover insights that matter most to LPs.

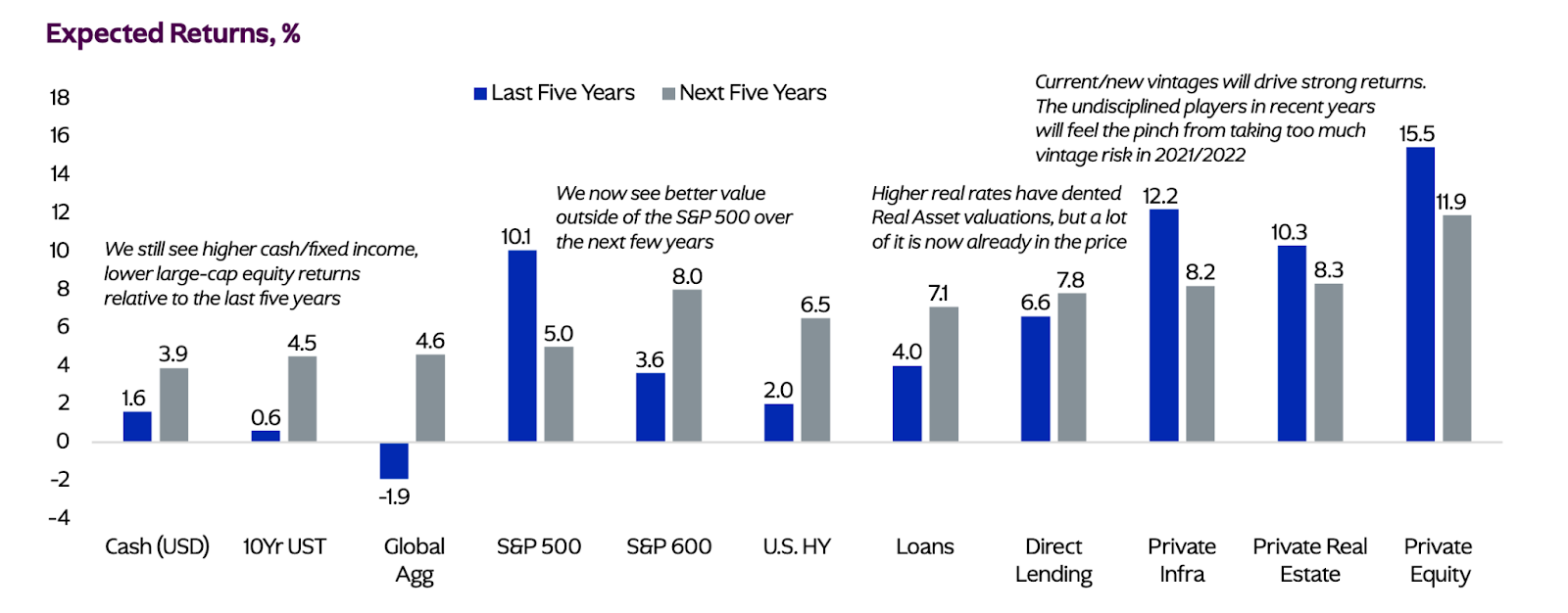

Current Vintages to Drive Strong Returns

In KKR’s latest report “How are We Thinking About Expected Returns”, expected returns in private equity over the next five years are expected to lower to 11.9% compared to the 15.5% seen in the previous five years, but this decline isn’t due to structural issues within the industry.

First, KKR still expected Private Equity to have the highest returns over the next five years out of the asset classes it looked at.

Second, current and new vintages are expected to drive high returns, as seen in the chart below, but the industry will see a drag from undisciplined PE investments made during the frenzy years of 2021 and 2022. Many GPs rushed to deploy capital during these years without proper due diligence, and these investments will strain the industry’s returns as they mature over the next five years.

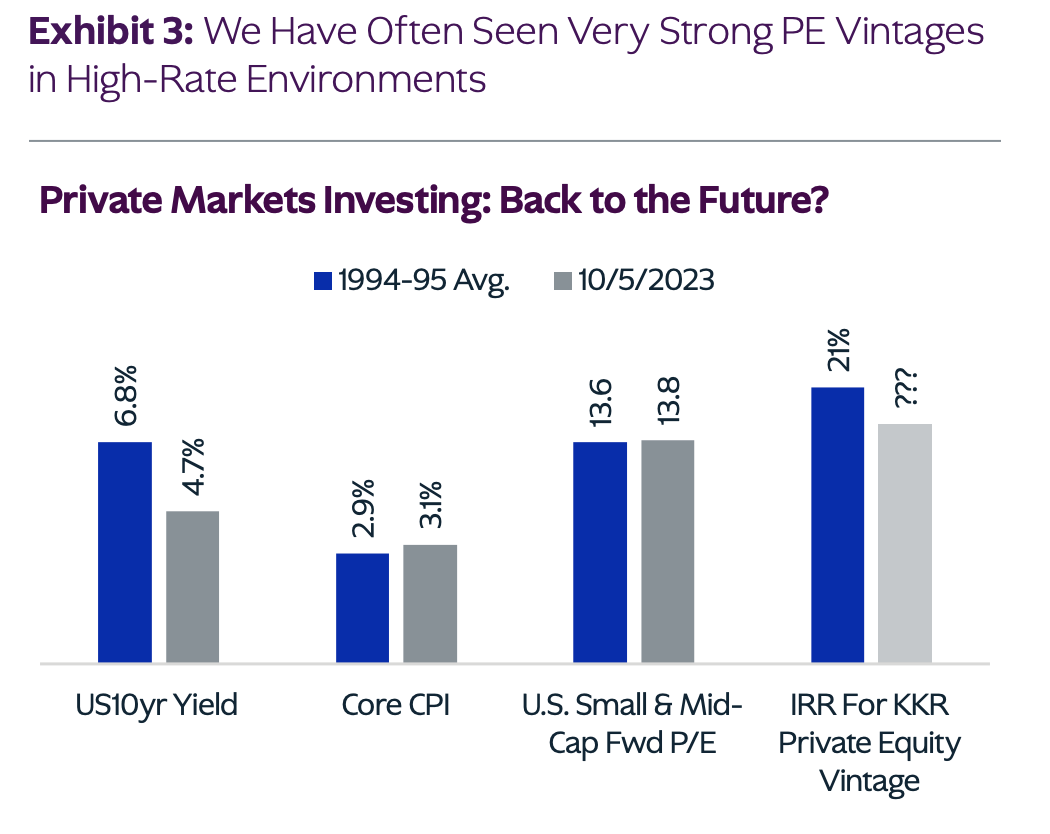

Ignoring lower-quartile performers, private equity is expected to retain optimal returns going forward in today’s environment and the industry could see strong vintages in the high-rate environment such as those in 1994-1995.

Structural Shifts in PE Investing

Now may be a good time to commit to new investments, but how can LPs prospecting new funds or secondaries forecast the success of potential GPs and avoid poor performers? A good start would be to assess how managers are thinking of PE’s key structural shifts outlined below:

Capital Structure:

The equity cushion in recent deals is higher than in the past, with the debt percentage of the total capital structure decreasing from around 40% in 2013 to 30% today.

Sophisticated sponsors have mitigated the impact of Fed policy decisions by extending debt maturities to smooth out changes. In addition, nearly 40% of managers have mitigated macro risks by hedging floating-rate interest exposure.

Overall, KKR predicts that the effect of Fed tightening on existing PE deals may be gradual, especially for GPs that manage leverage effectively. The pain will be felt by managers who took significant leverage when rates were near zero and did not hedge floating-rate debt.

Value Creation:

To offset the impact of higher rates, PE managers should focus on creating value through operational improvements, acquisitions, and strategic changes to offset the cash burn through higher rates. GPs that have more levers to achieve organic growth are positioned to outperform.

Private equity portfolio companies may have a strategic advantage over larger public firms, which have become too complex with multiple undermanaged subsidiaries. In this new era of private market investing, KKR believes there’s potential for significant PE-led carve-out transactions of the underperforming divisions of public conglomerates. This trend favors more experienced, sophisticated GPs.

Exit Multiples:

Theoretically, multiples should decrease with rising interest rates but public markets have shown a willingness to pay higher multiples for big, thematic, and simple companies.

GPs should be identifying areas where they can be a source of patient capital and partner with management teams to drive operational efficiency to command higher multiples in public markets. Examples of this are carve-outs and late-stage VC-backed firms that cannot find the capital required to scale.

How Should LPs Think Through this?

The bottom line is that existing and new private equity vintages may fare better than expected as interest rates and prices normalize. Current vintages have the potential for strong performance, with historical evidence supporting the productivity gains of de-leveraging cycles.

However, strong operational improvement, disciplined capital structures with ample equity cushion, collateral-based cash flows, and strategic exit strategies will be key to outperformance in this new environment. Manager selection will become more crucial than ever as skilled GPs outperform and more passive asset allocators see dwindling performance. LPs must consider whether GPs are adapting to the structural private market shifts discussed above.

Updates from Across the Ecosystem

Fundraising

Reports

GP perspectives:

Howard Marks (Co-Chairman, Oaktree)

Howard Marks’ new memo, “Easy Money” does an excellent job highlighting the structural shifts in our macroeconomic environment. I highly recommend reading the full memo, but in summary, the memo concludes that the era of easy returns in private markets is over.

Marks describes the previous low-interest rate environment as a moving walkway at the airport, where if you walk while on it, you move ahead faster than you would on solid ground. Almost all private market investors were profiting in the past decade due to the favorable macro conditions, whether they were truly skilled or not.

Now, only skilled GPs will continue making outsized returns in the high-rate market, making manager selection crucial. In addition, investors must watch out for the impacts of the “easy money” era, as the excessive risk-taking in those years may catch up to GPs in the coming years.

Andrew Schwedel, James Root (Partners, Bain)

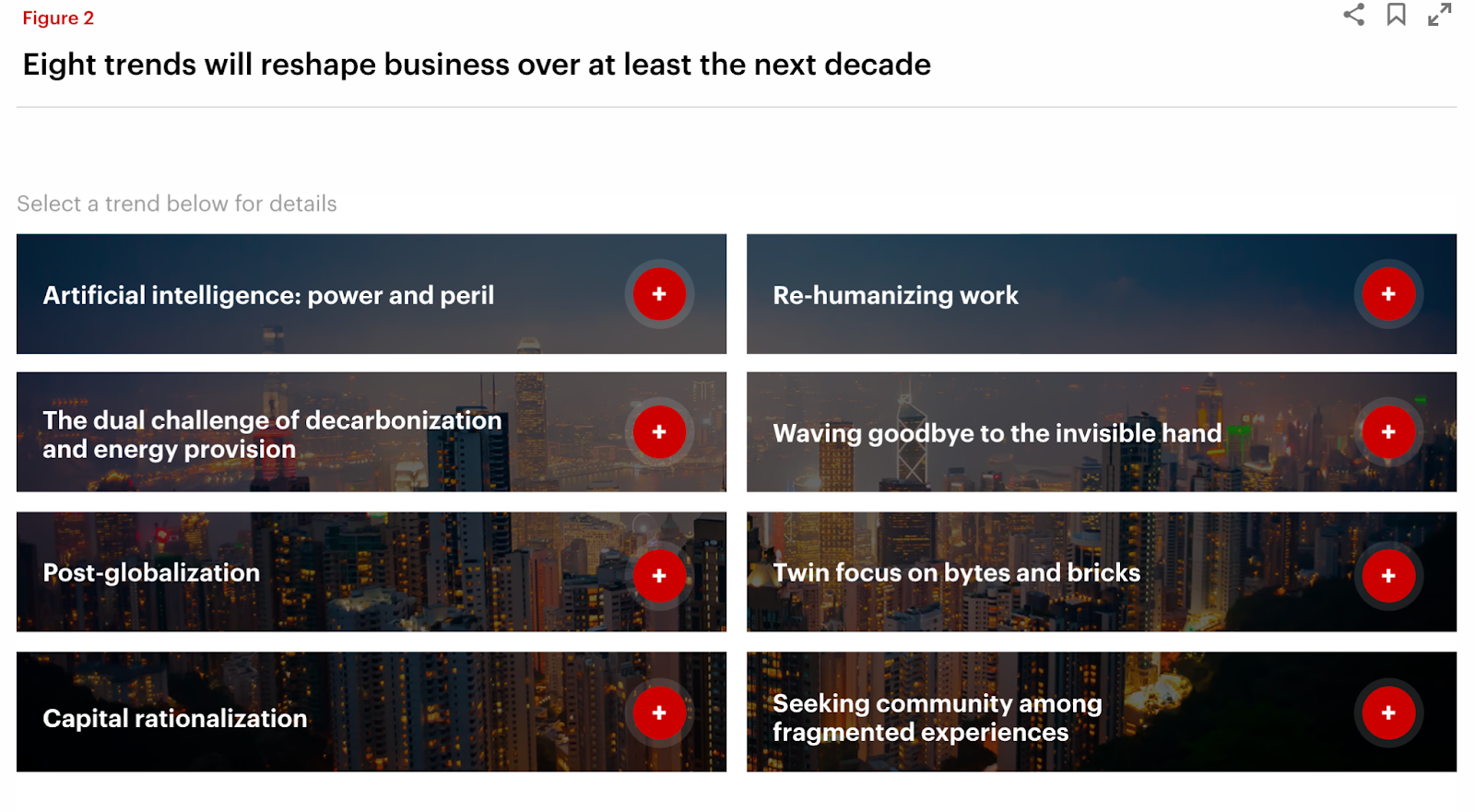

Bain partners Andrew Schwedel and James Root find that macro forces are accelerating in their latest market analysis. Currently, managers face a variety of challenges, from inflation, political unrest, and technological shifts like AI and traditional economic indicators no longer provide reliable predictions.

Despite these challenges, history shows that periods of disruption can lead to significant value creation and returns. The key lies in GP’s understanding and adapting to the changing landscape, considering both structural and cyclical changes. Bain highlights the following eight trends below as the most significant of this decade:

Overall, these trends will affect each sector differently, but Bain predicts a nuanced, multifaceted world where these themes converge, creating a complex dynamic across industries and markets. Understanding how these themes interact will unlock new opportunities.

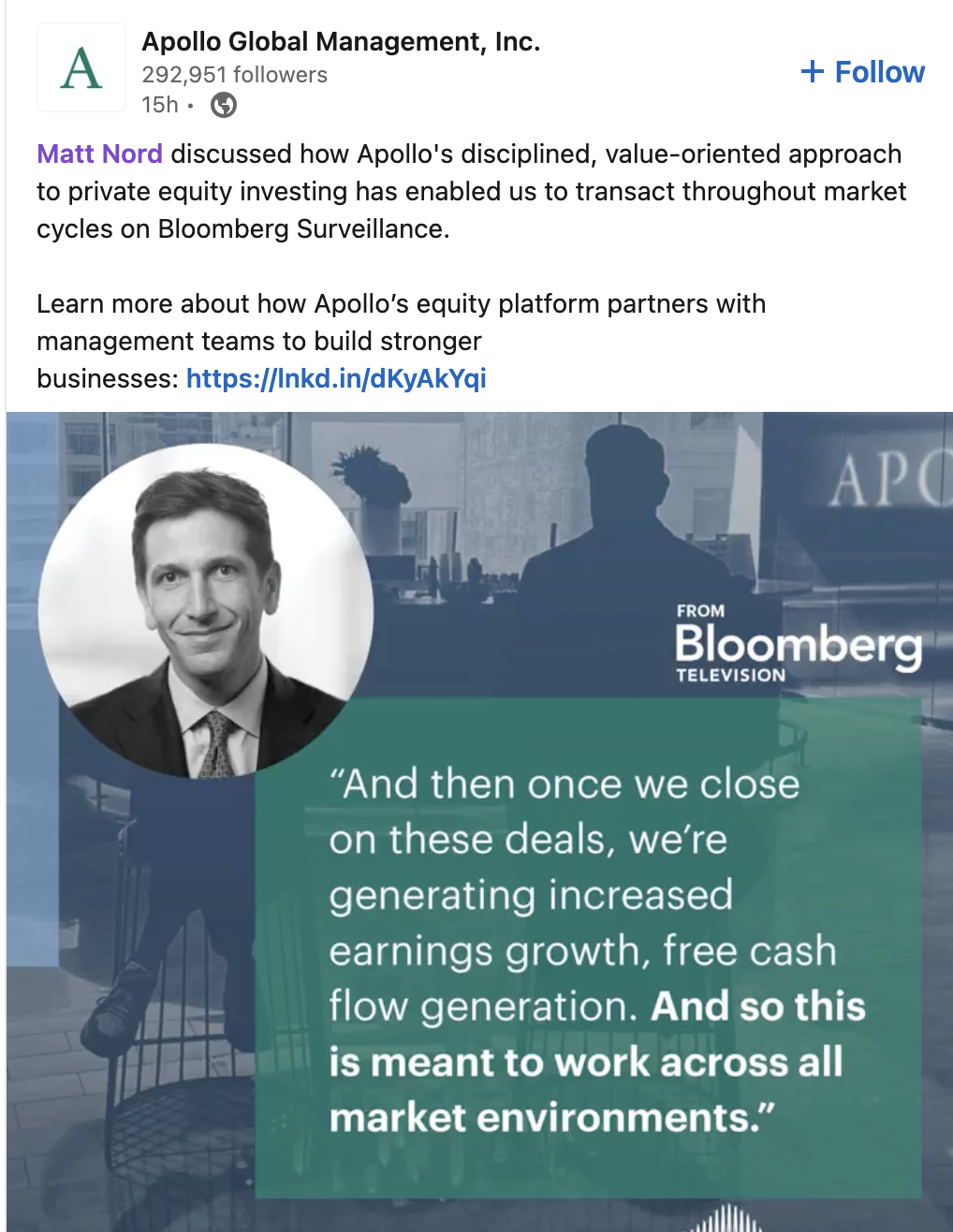

Matt Nord (Co-Head of Equity, Apollo Global Management)

Similar to the themes discussed in this newsletter, Matt Nord of Apollo acknowledges the shifts in our market environment. Apollo, like many other GPs, emphasizes a disciplined, value-oriented investing approach that focuses on basic metrics such as earnings growth, free cash flow generation, etc.

PEs like Apollo are reverting to the basics whereas they were promoting complex deal structures, financial engineering, and other sophisticated tools just a few years ago.

About OneFund

OneFund is democratizing access to Private Equity and Venture Capital for everyday investors. We partner with the world's top PE & VC funds to offer investment options without the million-dollar minimums.

If you would like to follow what we are doing, get more regular updates directly from the team, or become a member, schedule a call!

Reply