- Capital Call by OneFund

- Posts

- US PE Earnings

US PE Earnings

A bi-weekly newsletter from LPs for LPs, covering the latest and greatest from across the private markets

John Bailey

March 07, 2024

Calling all LPs! Thanks for joining me (John Bailey, Co-Founder at OneFund) for another edition of Capital Call.

The mission of Capital Call, our bi-weekly private equity newsletter from LPs for LPs, is to deliver concise, top-notch insights and updates from the private markets tailored to what matters for LPs.

This week we will be looking at:

US PE Earnings

Fundraising updates and Macro / Market reports

GP Perspectives from Henry McVey, Adam Parker, and Armen Panossian

Private Market Movements

US PE Earnings Update

In response to evolving market conditions, large US Private Equity funds are strategically repositioning themselves for growth. As the previous LBO boom fueled by cheap debt fades, leading GPs are pivoting to strategies that maintain momentum and expansion under new market conditions.

A priority for GPs in 2024 is growing their investor bases in preparation for potentially improving market conditions and M&A fueled by nearing rate cuts and a strengthening economy.

In this week’s newsletter I’ll dive into Pitchbook’s latest private equity dashboard to analyze GP performance and unpack the private market insights that matter most to LPs.

GPs Pivot to Targeting Individual Investors

The most notable shift in strategy over the past year is the search for new areas to attract capital. To achieve this, GPs have revealed new vehicles that allow a new class of investor to participate: individual investors.

Traditionally, PE investments have been dominated by institutional players, but many GPs are now raising substantial funds through their private wealth channels that aim to increase access to private-market assets.

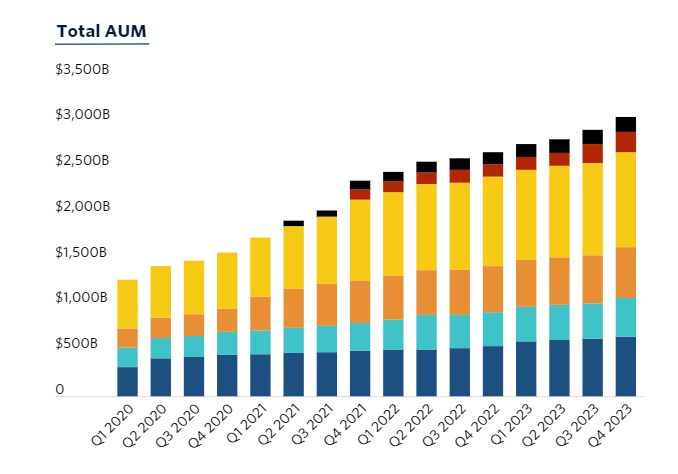

This is reflected in Pitchbook’s fundraising data. Using figures from public GPs as a market proxy, we see a steady rise of AUM across the market in 2023 despite poor conditions. Substantial capital inflows were seen in Q4 of 2023, and Pitchbook attributes this to new investors, as well as continued investment strength in certain categories.

Despite a broader PE slowdown, sectors such as credit investments, renewables, and infrastructure remain popular in attracting capital for GPs. These assets continue to provide a private investment-grade vehicle for investors seeking fixed-income substitutes, highlighting the resilience of credit-focused strategies in the current landscape.

Looking ahead, the industry will continue to focus on expanding the individual investor market as a new avenue of growth. GPs will be awarded with higher AUM while LPs gain the benefit of broader investment opportunities.

LPs should start rethinking portfolio diversification and rebalancing now to take into account the new opportunities available as private markets democratize.

Fees Expected to Rise as GPs gain Confidence

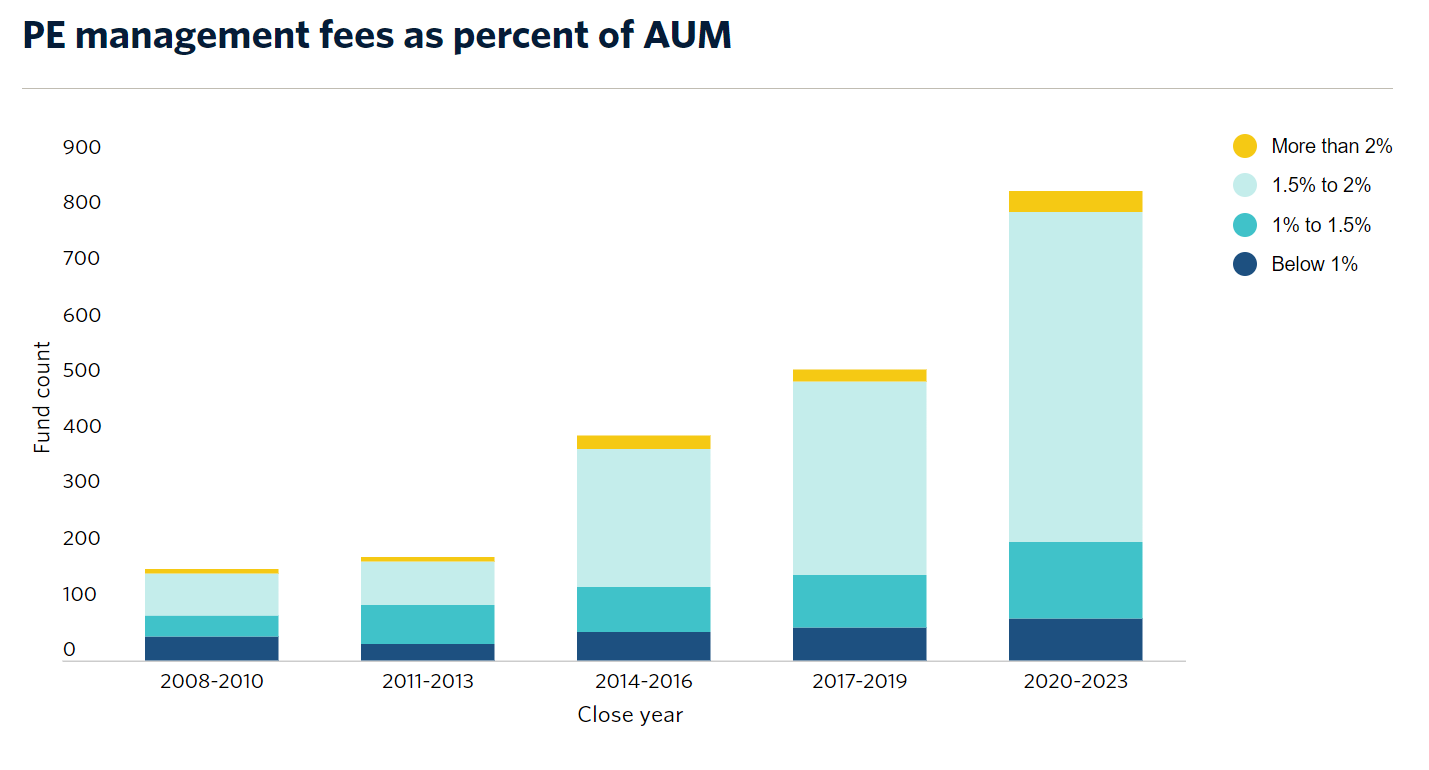

The investment landscape for PE appears optimistic, but LPs must watch out for expected management fee increases. According to Pitchbook, about 20% of GPs expect to increase firm fees in 2024 compared to just 5% in 2023.

This reflects the growing optimism in the industry that gives GPs more leverage to negotiate terms. As seen in the chart above, firms charging 1.5% to 2% and more than 2% are growing faster in number compared to sub-1% funds, and this trend is expected to continue growing.

LPs should expect a marginal rise in fees in future commitments and must model the impact fees have on overall returns. LPs should also ensure increased fees are backed by a compelling investment story, such as using fees to build out a stronger operations team, rather than merely following market trends.

Since fees can present a material drag on returns over the long run, LPs should scrutinize thoroughly to ensure that they are worth the cost.

Updates from Across the Ecosystem

Fundraising

Reports

GP perspectives:

Henry McVey (Head of Macro, KKR)

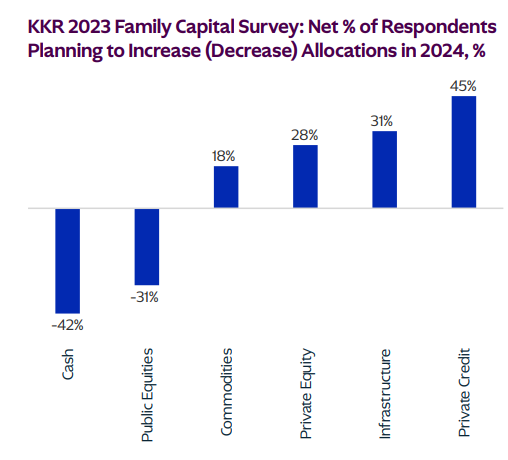

Henry McVey’s quote above reflects the growing impact of family office and individual investments for KKR’s growth, as GPs search for new areas to grow AUM.

In this year’s KKR survey of family offices, most plan to increase exposure to alternatives in 2024 as they hope to exploit the role illiquidity premium can play in compounding capital in a tax efficient manner.

Particular areas of focus for individual investors include Private Credit, Infrastructure, and Private Equity, as these areas tend to show low correlation with public markets. GPs hoping to fundraise successfully this year will need to offer investment vehicles targeting these markets.

For LPs, consider whether current cash positions are appropriate. KKR finds average family office cash positions at 9%, which McVey believes is unnecessarily high and brings down portfolio returns. Investors that consistently deploy capital throughout market cycles have been shown to outperform.

Adam Parker (CEO, Trivariate Research)

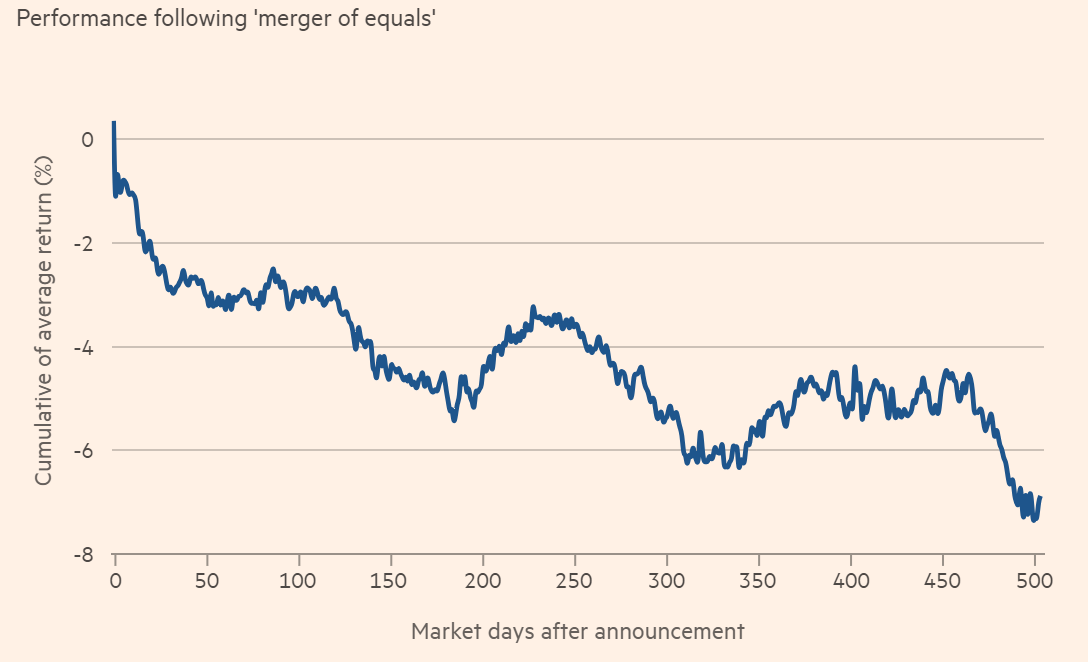

In a recent article, Adam Parker explains why mergers of equals often destroy value. LPs and GPs must consider his reasoning when considering whether to merge a portfolio company with one of similar size.

First, merging high-quality companies often leads to erosion of their fundamental edge due to mismanagement. On average, a high-quality company targeted in such mergers lags behind its industry group by 20% over the subsequent two years.

In addition, investors should be cautious about assuming synergies in these deals, as they often fail to materialize and can even lead to worse underperformance. For example, a different management team may not understand the culture, assets or competitive strengths of one business and destroy the advantages of the asset while trying to generate synergies.

Though mergers of equals can work in scenarios, investors should take caution. I recommend reading Adam’s full analysis for a full in-depth analysis.

Armen Panossian (Managing Director, OakTree)

While most investors anticipate rate cuts, Armen Panossian provides a contrarian view in a recent interview.

He believes that rate reductions are not made arbitrarily as they will only be used to promote full employment, inflation stability, and moderate economic growth. If this is already happening in the absence of cuts, the Fed may choose to observe without taking action.

Panossian suggests that recent events, such as the Fed's "transitory inflation" approach, favors higher rates to ensure effective control. Additionally, the proximity to an election year may influence the Fed's decision-making, with a preference for minimal intervention unless absolutely necessary to avoid perceptions of political influence.

Though the market consensus remains that rate cuts are imminent, investors cannot fully rely on them and must consider scenarios where they do not materialize.

Overall, LPs and GPs alike must retain a balanced view on investing. Fundraising is picking up as expectations brighten, but investors must not rush into fund commitments or M&A solely due to the positive outlook.

As always, a clear investment thesis with strong operational value drivers are needed to create value. Investors should also be preparing for downside scenarios where the market does not fully recover or rates remain high for an elongated period.

About OneFund

OneFund is democratizing access to Private Equity and Venture Capital for everyday investors. We partner with the world's top PE & VC funds to offer investment options without the million-dollar minimums.

If you would like to follow what we are doing, get more regular updates directly from the team, or become a member, schedule a call!

Reply